Pradhan Mantri Fasal Bima Yojana – Mid Term Appraisal

:Sandeepan

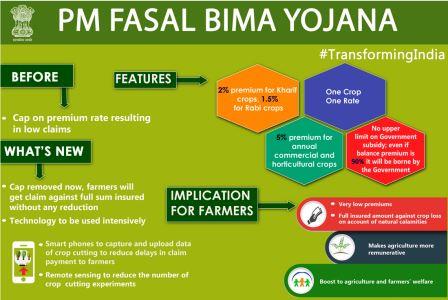

Features of Pradhan Mantri Fasal Bima Yojana

Pradhan Mantri Fasal Bima Yojana (PMFBY) was launched by the government in January 2016 to replace the existing two crop insurance schemes in India, National Agricultural Insurance Scheme (NAIS) and Modified NAIS. PMFBY was launched with the following features:

The scheme covers kharif, rabi crops and commercial and horticultural crops as well.

The premium charged for kharif crops would be up to 2% of the sum insured and for rabi crops it would be up to 1.5% of the sum assured.

For annual commercial and horticultural crops, the premium would be 5 per cent.

To provide insurance to the farmers at a subsidized rate of premium, the remaining share will be borne equally by the central and respective state governments.

This scheme will cover post-harvest losses also and provide farm level assessment for localised calamities including hailstorms, unseasonal rains, landslides and inundation.

To fasten the process of claims, the scheme proposes mandatory use of remote sensing, smart phones and drones for quick damage assessment.

Problems with NAIS and MNAIS

The NAIS and the MNAIS were not serving the farmers’ interests well and suffered from following lacunae:

- The sum insured under MNAIS, particularly for risky crops and districts, was meagre and was based either on the quantum of crop loans or on the capping of the sum insured.

- The crop damage assessment method based on crop cutting experiments was very slow and time-consuming.

- The time taken for compensation to reach the farmers often ran into several months.

Improvements via PMFBY

To overcome the problems and the weaknesses of the NAIS and MNAIS, the government decided to incorporate following essential elements in the new scheme:

A technical committee was proposed to be set up in each district to decide the scale of finance for the sum insured.

The premiums are to be decided on an actuarial basis which would give credibility to the process of setting premiums.

Bids are invited from public and private insurance companies to decide the premiums, thus adding an element of competition which would work in the favour of the farmers.

The farmers were required to pay the premiums at a subsidized rate and rest is paid by the government as mentioned above.

Use of technology such as smart phones, GPS, drones and satellites to ensure accuracy, transparency, and faster assessment of damages and settling claims.

Impact of PMFBY

To know the impact and the results achieved due to the introduction of this scheme, it is essential to know a few numbers in comparison to the erstwhile insurance schemes performance in Kharif 2013 and Kharif 2015.

- Farmers Insured

The number of farmers insured under the PMFBY rose by 193% over Kharif 2013 and by 0% over Kharif 2015. The number of non-loanee farmers also increased by more than six times.

- Area Covered

The area insured also increased from 16.5 million hectares (mha) in kharif 2013 and 27.2 mha in kharif 2015 to 37.5 mha under PMFBY.

- Sum Insured

The sum insured has witnessed a huge rise and has gone up from Rs 34,749 crores in kharif 2013 to Rs 60,773 crores in kharif 2015, and now to Rs 1,08,055 crores under PMFBY.

Challenges faced by PMFBY

PMFBY has also had its own share of challenges and shortcomings in terms of implementation. These need to be ironed out to ensure that the scheme serves the farmers well and at a lower cost. Few of the problems faced by PMFBY have been:

This scheme has witnessed an increase in the actuarial premium, instead of coming down with the increasing scale of coverage. A major reason for this is high price charged by various insurance companies to increase their profits. The competition in the upcoming seasons will reduce this rate of premium and reduce cost to the government.

Areas in eastern Uttar Pradesh, Bihar and Assam which faced floods and subsequent loss to farmers saw inspections being done by human eye.

Drones were not employed and smart phones which had to be issued to field officials, as per guidelines, were also not issued.

States failed to pay premiums to companies in advance in many cases.

There has also been a delay in compensating the farmers.

The scheme does not cover the risks and losses inflicted by wild animals like elephants and wild boars which is a major problem in certain states.

To conclude:

PMFBY has a lot of potential to tackle the impact of vagaries of nature on Indian agriculture.

At the rate at which it is increasing the coverage and the scope India may soon have half of its cropped area insured within three to five years. The subsidized premium for farmers is a big boost and will reduce farmer distress as well, although the scheme will increase the cost to the government.

Success of PMFBY depends on its sincere implementation and overcoming certain traditional problems faced by Indian agriculture such as poor land records, flawed land titles and corruption.